In the second scenario, revenueis included in the net income on the income statement, but the cashhas not been received by the end of the period. In both cases,current assets increased and net income was reported on the incomestatement greater than the actual net cash impact from the relatedoperating activities. To reconcile net income to cash flow fromoperating activities, subtractincreases in current assets. Cash flows from investing activities always relate to long-term asset transactions and may involve increases or decreases in cash relating to these transactions. The most common of these activities involve purchase or sale of property, plant, and equipment, but other activities, such as those involving investment assets and notes receivable, also represent cash flows from investing. Changes in long-term assets for the period can be identified in the Noncurrent Assets section of the company’s comparative balance sheet, combined with any related gain or loss that is included on the income statement.

How to Calculate Depreciation Expense: Straight Line Method

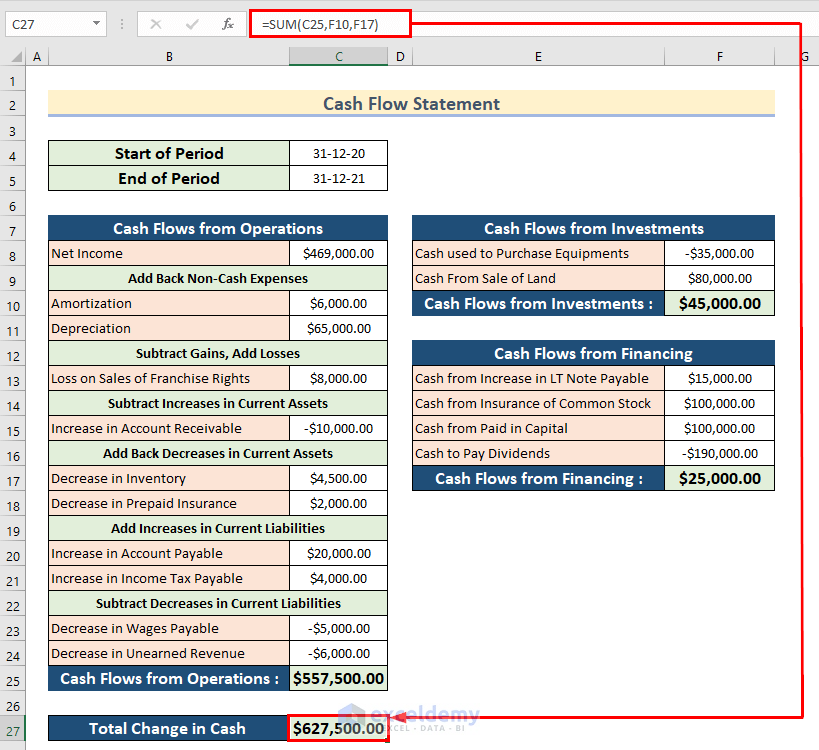

The purpose of a cash flow statement is to provide a detailed picture of what happened to a business’s cash during a specified period, known as the accounting period. It demonstrates an organization’s ability to operate in the short and long term, based on how much cash is flowing into and out of the business. This topic is examined in much more depth in the FR examination than it is at FA. For example, in FA, an extract, or the whole statement of cash flow might be required in the multi-task questions but it could also be constructed as an OT question. FR, however, is more likely to ask for an extract from the statement of cash flows using more complex transactions (for example, the purchase of PPE using right-of-use asset leases). However, that does not mean that FR will never require the preparation of a complete statement of cash flows so be prepared.

Part 2: Your Current Nest Egg

Operating activities are the main revenue-generating activities of a company and are central to its core business operations. Under the indirect method, the cash flow from operating activities starts with the net income from the income statement. This figure is then adjusted for non-cash expenses such as depreciation and amortization, as well as for deferred taxes. Changes in working capital accounts—such as accounts receivable, inventory, and accounts payable—are also factored in.

Do you own a business?

- Now the addition of Operating, Investing, and Financing activity figures will result in a cash balance of $906,000 (895,000+10000+1000).

- This adjustment ensures that the cash flow from operations is not overstated by the gain.

- Cash flow statements are one of the most critical financial documents that an organization prepares, offering valuable insight into the health of the business.

- Investors can determine a company’s profitability from the cash flow statement.

- The operating activities cash flow is based on the company’s net income, with adjustments for items that affect cash differently than they affect net income.

Therefore, it should always be used in unison with the income statement and balance sheet to get a complete financial overview of the company. Another important function of the cash flow statement is that it helps a business maintain an optimum cash balance. They can be calculated using the beginning and ending balances of various asset and liability accounts and assessing their net decrease or increase.

You will also make adjustments to changes in long-term assets and liabilities. The indirect method starts by taking the net income provided in the income statement. Investors, business leaders, and other stakeholders of the business are often interested in the operating section when doing a cash flow analysis. The content provided on accountingsuperpowers.com and accompanying courses is intended for educational and informational purposes only to help business owners understand general accounting issues. The content is not intended as advice for a specific accounting situation or as a substitute for professional advice from a licensed CPA.

This will typically involve your accounts payable and accounts receivable. But, if you’re building it manually, the components of the indirect method come directly from items reported on the other financial statements. So, you don’t need to seek out additional information in order to prepare the operating section of the income statement with this method.

To reconcile net income to cash flow from operating activities, subtract increases in current assets. Decreases in current assets indicate lower net income compared to cash flows from (1) prepaid assets and (2) accrued revenues. For decreases in prepaid assets, using up these assets shifts these costs that were recorded as assets over to current period expenses that then reduce net income for the period. Thus, cash from operating activities must be increased to reflect the fact that these expenses reduced net income on the income statement, but cash was not paid this period. Secondarily, decreases in accrued revenue accounts indicates that cash was collected in the current period but was recorded as revenue on a previous period’s income statement.

The Cash Flow Statement Indirect method is used by most corporations, begins with a net income total and adjusts the total to reflect only cash received from operating activities. For Propensity Company, beginning with net income of $4,340, andreflecting adjustments of $9,500, delivers a net cash flow fromoperating activities of $13,840. Investing net cash flow includes cash received and cash paidrelating to long-term assets. However, it is most useful when you’re trying to determine the ebbs and flows of your business’s cash flow. Most businesses prefer to use this method, since it shows cash flow in a more realistic sense. If you’re doing an internal audit of your cash flows, be sure to use the indirect method.

When a prepaid expense increases, the related operating expense on a cash basis increases. (For example, a company not only paid for insurance expense but also paid cash to increase prepaid insurance.) The effect on cash flows is just the opposite for decreases in these other current assets. The purpose of our cash flow is to reconcile cash so we will use the figure later. Decreases in current liabilities indicate a decrease in cash relating to (1) accrued expenses, or (2) deferred revenues. In the first instance, cash would have been expended to accomplish a decrease in liabilities arising from accrued expenses, yet these cash payments would not be reflected in the net income on the income statement.

This means that though Net Income is reported as decreased in the process, in reality – the cash has not been given out. In other words, an increase in a Current liabilities needs to be added back into income. Here’s a general rule of thumb when calculating the cash flow from Operations using the Cash Flow Statement Indirect Method. Simple Logic can be used to calculate the impact of an increase or decrease in Current Assets.

Cash flows from operating activities show the net amount of cash received or disbursed during a given period for items that normally appear on the income statement. You can calculate these cash flows using either the direct or indirect method. The direct method deducts from cash sales only those how to obtain a copy of your tax return operating expenses that consumed cash. This method converts each item on the income statement directly to a cash basis. Alternatively, the indirect method starts with accrual basis net income and indirectly adjusts net income for items that affected reported net income but did not involve cash.

Leave a Reply